")

Pavel Byrkin

Investment thesis

Being one of the major players in semiconductor industry, Advanced Micro Devices (NASDAQ:AMD) is well positioned to absorb significant part of growing demand for high-performance graphics and computing products. In recent years, the management demonstrated its ability of improving cash flows and diversifying company’s business by strategic acquisitions .

All in all ,the company has firm market position and experienced management with strong track record of innovation together with solid financials which makes it an attractive investment opportunity. Although we are currently experiencing challenging macro environment, my valuation model outcomes suggest an immense upside potential in the long-run, which by far outweighs possible risks.

Company information

AMD is one of the leading semiconductor companies which designs and manufactures computing and graphic high-performance hardware. The company is a top player in graphic processors [GPU] after acquisition of ATI in 2008. As part of AMD’s growth strategy the company is benefiting from integration with Xilinx, which was acquired in 2021, and enables AMD to expand its presence in embedded computing and data center segments.

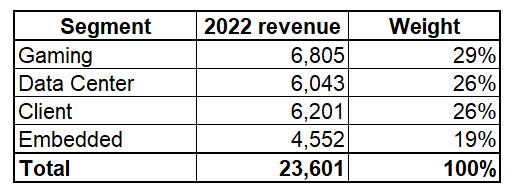

The company’s revenue comprises of four segments: Data Center, Client, Gaming and Embedded.

Author’s calculations

Financials – growth has been stellar

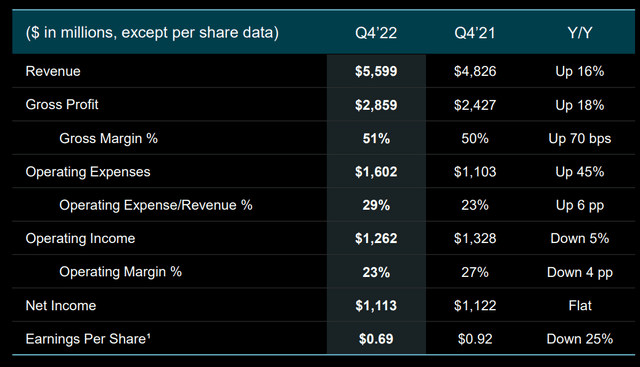

The company reported 4Q2022 financial statements on January 31, 2023. Results demonstrated a beat of consensus estimates both in terms of top line and EPS.

AMD

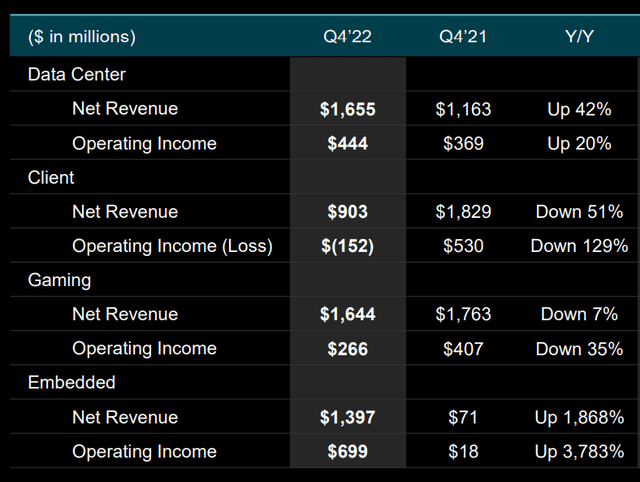

Increase in revenue in 4Q2022 was mainly generated by strong growth in Data Center and Embedded which was partially offset by Client PC segment being halved down and single-digit percentage decrease in Gaming segment.

AMD

Increase in Data Center revenue is primarily related to growing EPYC server CPU product line. Skyrocket growth in Embedded segment mainly represents non data center sales from Xilinx acquisition, which was completed in early 2022. Client computing sales big decline was caused by weaker demand and growing inventories. Morningstar Premium expects PC units to be down at least 10% in FY 2023. Gaming revenues declined slightly mainly because of lower GPU sales which were partially offset by growing console chip demand. GPU sales are largely dependent on cryptocurrency mining activity which I expect to be weak in 2023 due to multiple unfavorable external factors for crypto-industry. Overall, to finalise about quarterly P&L, non GAAP gross margin expanded 70 basis points due to efficient product mix of Data Center and Embedded segments sales.

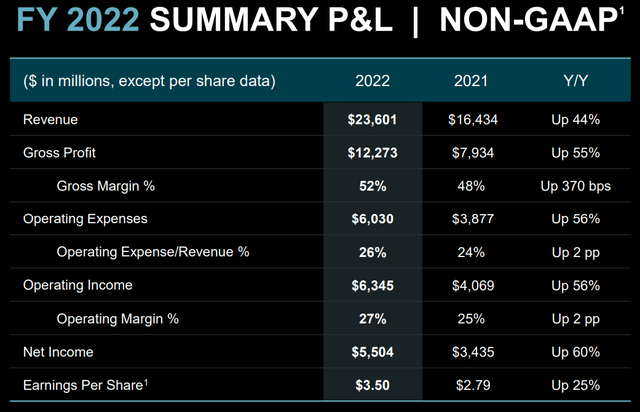

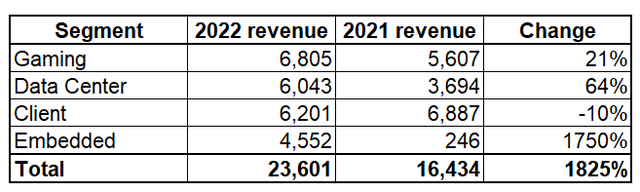

As for the full FY 2022 the company’s revenue increased 44% from $16.4 billion to 23.6 billion. This strong revenue growth contributed to a 25% growth in non-GAAP EPS.

AMD

Embedded and Data Center segments together were major contributors to full year revenue growth demonstrating growth from $3.9 billion in 2021 to $10.6 billion in 2022 following Xilinx acquisition two years ago.

Author’s calculations

Based on such a tremendous growth in Embedded segment we can see that Xilinx integration is run very well, making Embedded the major growth driver for company’s full year revenue. Here management proved itself as being strong in enhancing company’s financial model by diversifying the business. And synergies, are not over yet, during last earnings call the CEO said following regarding Xilinx:

In addition, we are seeing substantial new revenue synergy opportunities as we combine Xilinx’s industry-leading adaptive products and 6,000-plus customers with AMD’s expanded breadth of compute products and scale.

Management also provided an outlook for the full FY 2023. Overall, they expect FY 2023 to be mixed with second half of the year much stronger than the first one mainly due to elevated inventory levels at the reporting date. Data Center and Embedded segments are expected to grow YoY with gross margin expanding in the second half of the year across all segments.

According to Dr. Lisa Su, the CEO, in next year’s rapid growth in Artificial Intelligence [AI] adoption will become one of major drivers for company’s further growth:

We expect AI adoption will accelerate significantly over the coming years and are incredibly excited about leveraging our broad portfolio of CPUs, GPUs and adaptive accelerators in combination with our software expertise to deliver differentiated solutions that can address the full spectrum of AI needs in training and inference across cloud, edge and client.

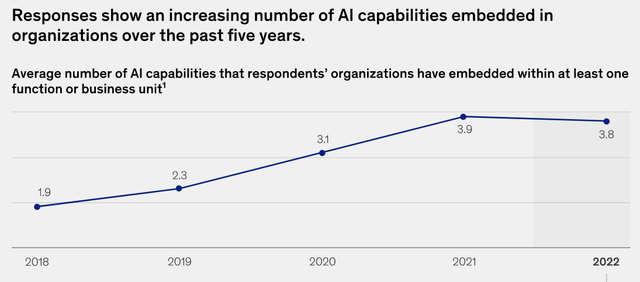

While researching evidence for the above thesis of the company’s CEO, I found some interesting data on AI from McKinsey. The figure I found most interesting is the fact that within last 5 years the number of AI capabilities that businesses used, has doubled, which indicates aggressive pace of AI adoption:

McKinsey

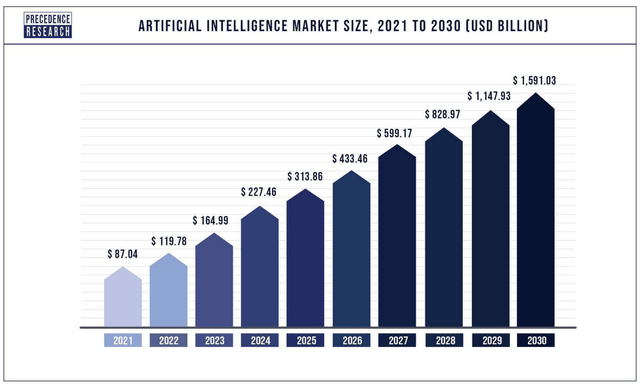

To proceed with more forward-looking view on the matter, Precedence Research forecasts that by the year 2030 AI market will increase tenfold from current levels, which is huge.

Precedence Research

From a balance sheet perspective things are also going well, we can see that at the reporting date, the net cash position is strong, which enabled the company to return $3.7 billion to shareholders via share repurchases in FY 2022.

To sum up this part, AMD’s financial position is strong and company’s financial performance and next year’s outlook evidences that management is highly likely to be able to deliver further shareholders’ wealth growth.

Valuation

Seeking Alpha’s Quant Ratings assess AMD’s valuation attractiveness as not very high which is evidenced by a “C-” valuation grade. But, I see huge upside potential here and I would like to prove my opinion with the analysis and calculations below.

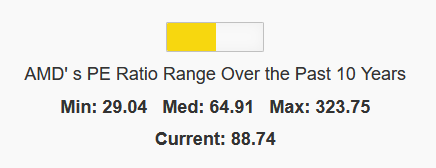

First, from multiples perspective, the stock is significantly undervalued because it is currently trading at forward P/E of 17.83 which is well below company’s last 10-year’s lowest point of 29.04.

Gurufocus

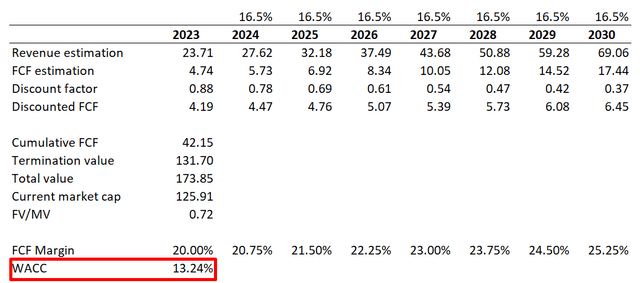

To calculate fair value I prefer discounted cash flow model [DCF] here since AMD is a growth stock and it’s valuation depends heavily on future cash flows. Using sound WACC for discounting is crucial, so I refer to NYU Stern as a source, which currently evaluates semiconductor hardware industry’s cost of capital at 13.24%. Free cash flows [FCF] I expect at rather conservative 20% of revenues growing 75 basis points each year. I consider it conservative because the company already demonstrated ability to generate 19% FCF margin and it is highly likely that economies of scale will be effectively utilised by the company’s management. Revenue CAGR I expect at 16.5% between 2023 and 2030 which represents a rather modest growth rate if compared to the latest Report Insights where a 33.5% CAGR is forecasted for Graphic Processors market growth.

Incorporating all assumptions together the DCF valuation exercise suggests that the stock is almost 30% undervalued.

Author’s calculations

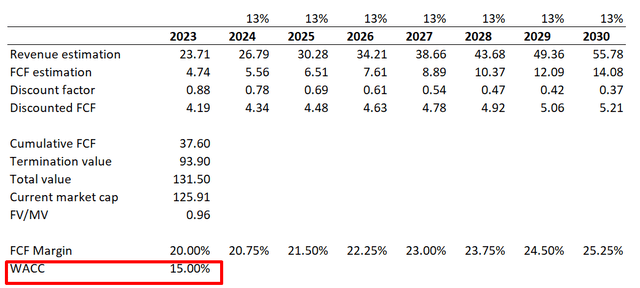

Let’s also not forget that in 2023 we are close to peak in the Fed rates tightening cycle. Easing Fed rates would cause decline in cost of capital for companies, so WACC will follow inevitably. Therefore it would be a useful exercise to check DCF sensitivity to changes in WACC.

In case Fed rates go through few more hikes, WACC for AMD could highly likely move above 14%, so to be conservative I select 15% for this sensitivity test. It is also obvious that higher Fed rates will hit demand for technology hardware so here I also cut my revenue growth expectations to 13%. After WACC and revenue growth assumptions changed the model suggests that the stock is still undervalued.

Author’s calculations

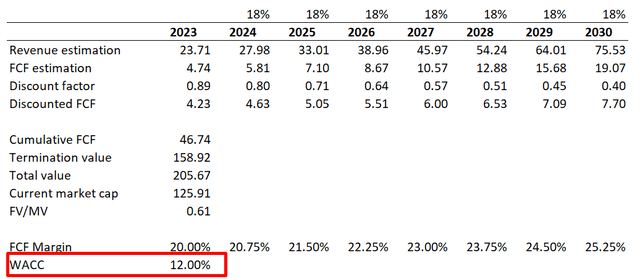

For second part of sensitivity analysis, which scenario I believe is more likely, we should calculate how rates easing will affect fair value of AMD. According to Charlie Bilello, rates are expected to start easing in late 2023 with easing cycle terminating (or pausing) at about 3.5% in early 2025. If Fed rates go to 3.5% I believe that for AMD WACC 12% would be a reasonable level together with 18% revenue CAGR expected.

Author’s calculations

According to this optimistic scenario, the stock is almost 40% undervalued. And me personally, in long-term I see optimistic scenario as most likely for AMD.

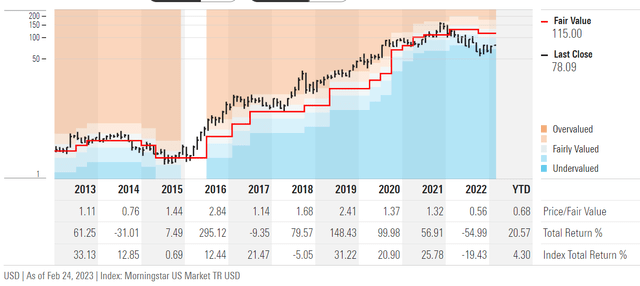

To conclude valuation exercise, DCF calculations given conservative assumptions together with multiples analysis suggest that there is a massive upside potential for the stock and margin of safety is also in place. To check myself, I also analysed Morningstar Premium’s opinion on the stock fair value and they are even more optimistic than me indicating almost 50% upside potential with stock’s fair price at $115. Below you can see the chart indicating that usually AMD’s actual stock price follows Morningstar’s fair value estimates in long-term horizon.

Morningstar Premium

Potential risks

Despite the fact that AMD represents a compelling investment opportunity, investors should also consider risks attributable to investing in AMD.

In current times I think that possible economic recession is a major risk, because it will lead technology hardware sales to plunge. On the other hand it is highly likely that AMD’s strong balance sheet and sustainable cash flows will enable company to endure this possible economic hurricane.

Second major risks which I see is high competitiveness of semiconductor industry and pace of innovation. All technology companies face risk of becoming obsolete and fail to keep up with competitors. But, at the same time, the company’s CEO, Dr. Lisa Su, who took over in 2014, together with the management team, has strong track record of delivering stellar growth and high profitability margins.

Seeking Alpha

Third big risk that I see is the fact that AMD is very integrated in the whole global technology ecosystem heavily depending on major IT companies like Amazon, Microsoft or Google as well as the regulation on information technology which can possibly be tightened and that may impose risks on company’s future growth and profitability.

Bottom line

In summary, I have high conviction that the current levels of AMD share price do not fully reflect the company’s potential for revenue growth and margin expansion. Given current favorable valuation metrics, the stock is a strong buy with significant upside potential which outweigh risks and current challenging macro environment headwinds.

link